Why may the auditor use a different performance materiality amount or percentage of account balance for some financial statement accounts?

Review Exhibits 1 and 2; audit memos G-3 and G-4; and audit schedules G-5, G-6 and G-7. Based on your review, answer each of the following questions:

The objective of an audit is to provide reasonable assurance that the client's financial statements are

fairly presented in all material respects at the lowest possible cost. A lower performance materiality

may be required for specific accounts because of the relevance of the account to users. The lower the

performance materiality for an account the more evidence and cost that will be needed to audit the

account. Conversely, the higher the performance materiality for an account the less evidence and cost

that will be needed to audit the account. Therefore, to minimize cost, auditors will only want to assign

a lower performance materiality to accounts more relevant to users.

You might also like to view...

(Appendix) Payments to employees and to the government are examples of cash outflows resulting from operating activities

a. True b. False Indicate whether the statement is true or false

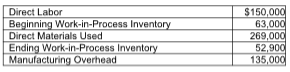

During the year, Velasco produced 71,220 units of product. Calculate the unit product cost. (Round your answer to the nearest cent.)

Velasco Productions has provided the following information for the year:

A) $7.92

B) $6.77

C) $7.78

D) $8.66

Two barriers to discovering vocation are ______.

A. forgetfulness and avoidance B. anger and pride C. ambition and avoidance D. time pressures and lack of guidance

__________ can include boycotts of goods, refusal to maintain commercial relationships, and quotas

a. Economic sanctions b. Embargoes c. Tariffs d. Dumping