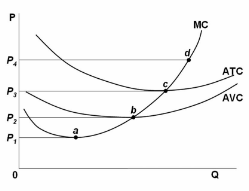

Refer to the diagram for a purely competitive producer. The lowest price at which the firm should produce (as opposed to shutting down) is:

A. P 1 .

B. P 2 .

C. P 3 .

D. P 4

B. P 2 .

You might also like to view...

A firm's marginal cost is $30, its average total cost is $50, and its output is 800 units. Its total cost of producing 801 units is

A) less than $40,000. B) between $40,000 and $40,050. C) between $40,050 and $40,080. D) greater than $40,080.

A perfectly competitive industry achieves allocative efficiency in the long run. What does allocative efficiency mean?

A) Firms use an input combination that minimizes cost and maximizes output. B) Each firm produces up to the point where all scale economies are exhausted. C) Each firm produces up to the point where the price of the good equals the marginal cost of producing the last unit. D) Production occurs at the lowest average total cost.

The human costs of unemployment are

a. insignificant b. not as important as the economic costs of unemployment c. equal to the economic costs of unemployment d. not measured in dollars, but are extremely important considerations e. the opportunity cost of lost output

Which of the following statements is NOT consistent with new growth theorists' beliefs?

A. Innovation can lead to lower productivity costs. B. Technology must be understood in terms of what drives it. C. Rewards lead to technological advances. D. Inventions are much more important than innovation.