When something happens to the economy, monetarists ask two questions:

A. What does this do to government spending, and what does it do to tax revenues?

B. What does this do to real GDP, and what does it do to the price level?

C. What does this do to investment spending, and what does it do to net exports?

D. What does this do to the money supply, and what does it do to velocity?

Answer: D

You might also like to view...

If nation-states are able to extend effective control over ocean resources from 3 miles to 200 miles off their coasts, valuable marine animals are more likely to be harvested

A) at a rate consistent with their long-run preservation. B) at a rate inconsistent with their long-run preservation. C) too rapidly for maximum net benefit. D) too slowly for maximum net benefit. E) up to the point of extinction.

When there are large network effects of adopting a new technology, firms often feel that government regulation or joint ventures can solve the

A. problem of excess capacity. B. market inefficiency problem. C. coordination problem. D. problem of excessive investment.

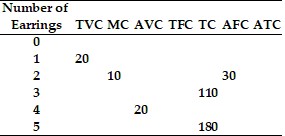

Refer to the information provided in Table 8.3 below to answer the question(s) that follow.

Table 8.3 Refer to Table 8.3. What is the total cost of producing zero units of output?

Refer to Table 8.3. What is the total cost of producing zero units of output?

A. $0 B. $30 C. $60 D. indeterminate from the given information

Assume a perfectly competitive industry is in long-run equilibrium at a price of $150. If this industry is an increasing-cost industry and the demand for the product increases, long-run equilibrium will be reestablished at a price

A. of $150. B. greater than $150. C. less than $150. D. either greater than or less than $150 depending on the magnitude of the decrease in demand.