In perfect competition, marginal revenue, average revenue, and ______ are all equal.

a. percentage revenue

b. quantity

c. total revenue

d. price

d. price

You might also like to view...

There is a technological advance in a perfectly market. Which of the following statements is NOT true?

A) As more firms begin to use the new technology, the market supply increases and the price falls. B) Technological change brings permanent gains to producers and temporary gains to consumers. C) In the new long-run equilibrium, all the old-technology firms have exited. D) In the long-run equilibrium, competition eliminates any short-run economic profit.

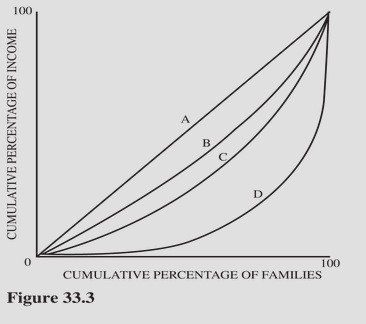

Figure 33.3 illustrate four different Lorenz curves. Assume Brazil has a larger Gini coefficient than the United States. If the income distribution for the United States is represented by curve C, which curve would must represent the income distribution for Brazil?

Figure 33.3 illustrate four different Lorenz curves. Assume Brazil has a larger Gini coefficient than the United States. If the income distribution for the United States is represented by curve C, which curve would must represent the income distribution for Brazil?

A. A. B. B. C. C. D. D.

The knowledge and skills acquired by a worker through education and experience is a description of which factor of production?

A. physical capital B. human capital C. labor D. entrepreneurship

What are the ingredients of growth?

What will be an ideal response?