Refer to Figure 3-6. The figure above represents the market for coffee grinders. Assume that the market price is $21. Which of the following statement is true?

A) There is a shortage that will cause the price to increase; quantity demanded will then decrease and quantity supplied will increase until the price equals $25.

B) There is a shortage that will cause the price to increase; quantity supplied will then decrease and quantity demanded will increase until the price equals $25.

C) There is a shortage that will cause the price to decrease; quantity demanded will then increase and quantity supplied will decrease until the price equals $25.

D) There will be a shortage that will cause the price to increase; demand will then decrease and supply will increase until the price equals $25.

A

You might also like to view...

The short-run supply curve for a perfectly competitive firm is its marginal cost curve above the minimum point on the

A) average fixed cost curve. B) average variable cost curve. C) average total cost curve. D) demand curve.

In practice, oligopolistic markets are:

A. fairly common. B. very rare. C. forbidden by the government. D. usually protected by the government.

The concept of marginality is important in economics because

A. marginal decisions indicate a lack of importance. B. individuals make decisions at the margin. C. large expenditures are the only factor influencing consumption. D. individuals make decisions based on tastes only.

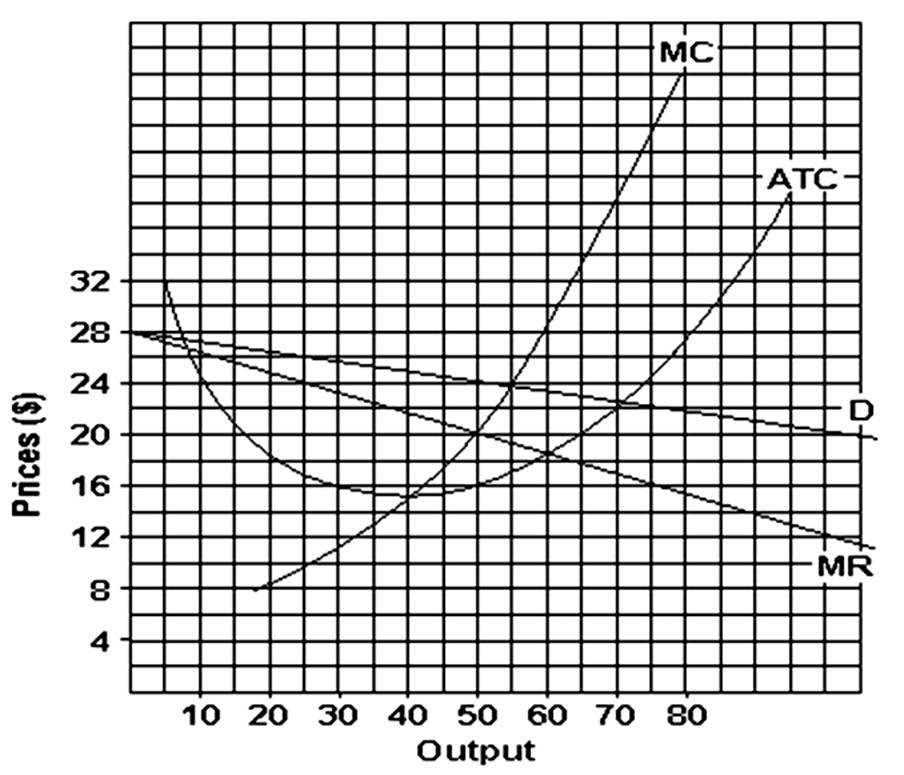

You could conclude that

A. new firms will enter the industry.

B. existing firms will leave the industry.

C. existing firms will continue to make a profit, even in the long run.

D. new firms will leave the industry.