For a monopolistically competitive firm in long run equilibrium:

a. marginal revenue equals marginal cost and price equals average cost

b. the economic profits it is earning will soon be competed away by entry.

c. accounting profits are zero and price equals marginal cost.

d. marginal revenue equals marginal cost and average total cost is minimized.

a

You might also like to view...

You are given the following market data for apples

Demand is represented by: P = 12 - 0.01Q Supply is represented by: P = 0.02Q where P= price per bushel, and Q=quantity. a. Calculate the equilibrium price and quantity. b. Suppose the government guaranteed producers a price of $10 per bushel. What would be the effect on quantity supplied? Provide a numerical value. c. By how much would the $10 price change the quantity of apples demanded? Provide a numerical value. d. Would there be a shortage or surplus of apples? e. What is the size of this shortage or surplus? Provide a numerical value.

Measuring unemployment is the job of the Bureau of Labor Statistics

a. True b. False Indicate whether the statement is true or false

In year 1 the CPI is 181, and in year 2 the CPI is 195. If Dennis's salary was $95,000 in year 1, what is the minimum salary he must earn in year 2 to "keep up with inflation"?

A) $112,500 B) $102,348 C) $105,750 D) $88,180

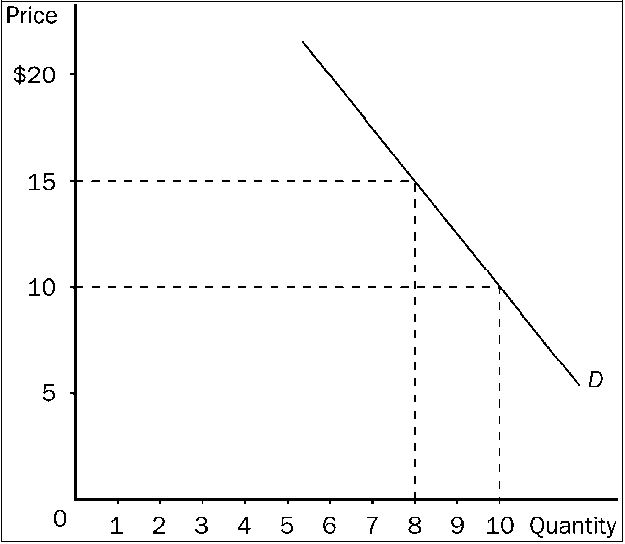

Figure 7-13

Refer to . If price increases from $10 to $15, total revenue will

a.

increase by $20, so demand must be inelastic in this price range.

b.

increase by $5, so demand must be inelastic in this price range.

c.

decrease by $20, so demand must be elastic in this price range.

d.

decrease by $10, so demand must be elastic in this price range.