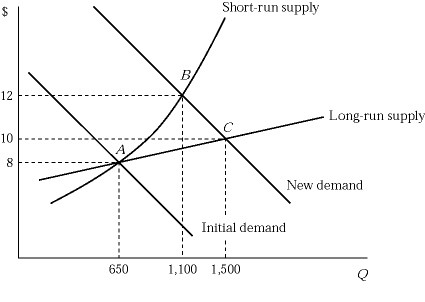

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

Figure 9.5Figure 9.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

A. The market price drops below $12 as more firms enter the market and build more plants.

B. Both existing firms and new firms earn a zero economic profit.

C. All firms in the industry maximize their profits by producing the output where the marginal cost equals $10.

D. All of these are correct.

Answer: D

You might also like to view...

Compared to other countries, the United States has a relatively low share of consumption spending in GDP

Indicate whether the statement is true or false

When you see a mansion and think to yourself that it must be worth a million dollars, you are using money to perform which function?

A) medium of exchange B) unit of account C) store of value D) means of payment E) method of avoiding barter

If left to market forces, activities that produce external benefits wil be over-produced

a. True b. False

A firm in a perfectly competitive market can maximize its profits by producing:

A. the level of output where marginal cost equals marginal revenue. B. any level below where marginal cost equals marginal revenue. C. any level beyond where marginal cost equals marginal revenue. D. slightly below its maximal capacity.