Why is the equilibrium price the best deal available for both buyers and sellers?

What will be an ideal response?

The equilibrium price reflects that the highest price consumers are willing to pay for that amount of the good or service and is just equal to the minimum price that suppliers require for delivering it. Demanders would prefer to pay a lower price, but suppliers are unwilling to supply that quantity at a lower price. Suppliers would prefer a higher price, but demanders are unwilling to pay a higher price for that quantity. Hence neither demanders not suppliers can do business at a better price.

You might also like to view...

The Coinage Act of 1792 set the relative values of silver and gold coins at 15 to 1 . Suppose the relative market values of silver and gold had equaled 16 to 1 . In this case,

a. only gold would circulate as money. b. gold would be hoarded and sold abroad. c. gold would be overvalued at the mint. d. individuals would profit by selling gold to the mint.

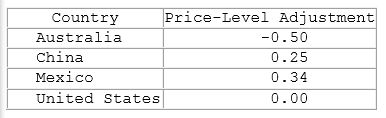

According to the information in the table shown, if someone were to make $35,000, she would be able to buy the most goods and services if she lived in:

This table shows the price-level adjustment as compared to the United States.

A. Australia.

B. the United States.

C. Mexico.

D. China.

If the economy is producing Natural Real GDP, then the

A) current unemployment rate is greater than the natural unemployment rate. B) current unemployment rate is less than the natural unemployment rate. C) economy is at full employment. D) economy is operating at the natural unemployment rate. E) c and d

Ceteris Paribus

What will be an ideal response?