Distinguish between static and flexible budgets. Give an example of how flexible budgets can be used.

What will be an ideal response?

Answers will vary.

Static budgets are based on a single estimate of volume, whereas flexible budgets show estimated costs and revenues at a variety of activity levels. Both types of budgets are based on the same per-unit standard amounts and the same fixed costs. Flexible budgets can be used for planning and performance evaluation. For example, managers may be able to evaluate the adequacy of the company's cash position by assuming different levels of activity. Similarly, the number of employees, the amounts of materials, and the necessary equipment and storage facilities can be evaluated at different potential activity levels to ensure the company is adequately prepared for whatever actual volume level occurs. After the period, flexible budgets can be prepared for the actual volume and used to evaluate cost control.

You might also like to view...

The depreciation method that does notuse residual value in calculating the first year's depreciation expense is

a. straight-line b. units-of-output c. double-declining-balance d. none of the above

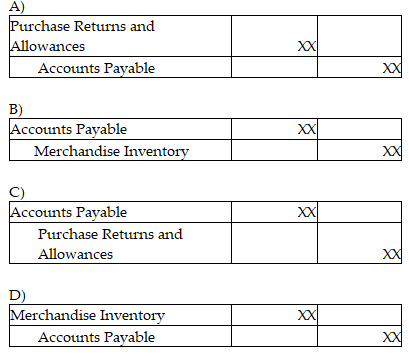

Which of the following is the correct journal entry for a return of goods that were purchased on account under the periodic inventory system?

Evaluating statistical sample results is one of the tasks that can be performed by GAS

a. True b. False Indicate whether the statement is true or false

Answer the following statements true (T) or false (F)

All influence that an individual experiences comes from influential external leaders.