Suppose that the salary range for recent college graduates with a bachelor's degree in economics is $30,000 to $50,000, with 25 percent of jobs offering $30,000 per year, 50 percent offering $40,000 per year and 25 percent offering $50,000 per year and that in all other respects, the jobs are equally satisfying. Assume that in this market, a job offer remains open for only a short time so that continuing to search requires an applicant to reject any current job offer. Who will accept an offer of $30,000?

A. Graduates who are risk-averse

B. Graduates who are either risk-neutral or risk-averse

C. Graduates who have been searching the longest

D. Graduates who enjoy taking risks

Answer: A

You might also like to view...

While in school, Kiki spends 20 hours a week as a computer programmer for Microsoft and studies 30 hours a week

A) Kiki is classified as a full-time worker, working 50 hours a week. B) Kiki is classified as a part-time worker, working 30 hours a week. C) Kiki is classified as a part-time worker, working 20 hours a week. D) Because Kiki is a student, she is not classified as working. E) Because Kiki is a student, she is classified as a full-time worker, working 20 hours a week at a paid job.

Which of the following components of the current account are included in GDP?

A) net exports B) net foreign investment income C) net transfer payments sent to foreigners D) all of the above

If a firm in a perfectly competitive industry is experiencing average revenues greater than average costs, in the long-run

a. Some firms will leave the industry and price will rise b. Some firms will enter the industry and price will rise c. Some firms will leave the industry and price will fall d. Some firms will enter the industry and price will fall

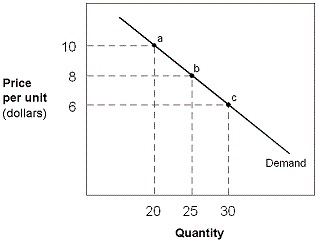

Exhibit 5-1 Demand curve

?

If demand price elasticity is 2, consumers would:

If demand price elasticity is 2, consumers would:

A. buy twice as much of the product in response to a 10 percent decrease in prie. B. require a 2 percent drop in price to increase their purchases by 1 percent. C. buy 2 percent more of the product in response to a 1 percent decrease in price. D. buy twice as much of the product in response to a 1 percent decrease in price.