Reported GDP increases when, in fact, total production is unchanged when I. there is a shift from household production to market production. II. a previously illegal activity is legalized

A) I only

B) II only

C) neither I nor II

D) both I and II

D

You might also like to view...

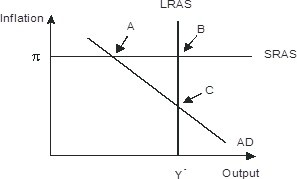

Refer to the figure below.________ inflation will eventually move the economy pictured in the diagram from short-run equilibrium at point ________ to long-run equilibrium at point ________.

A. Rising; A B. Falling; A; C C. Falling; B: C D. Rising; A; C

On a production possibilities frontier, 500 pounds of apples and 1,200 pounds of bananas can be produced while at another point on the same frontier, 300 pounds of apples and 1,300 pounds of bananas can be produced

Between these points, what is the opportunity cost of producing a pound of apples? A) 2 pounds of bananas B) 5/12 of a pound of bananas C) 0.5 of a pound of bananas D) 2 pounds of apples E) 100 pounds of bananas

Compared to the case in which a monopoly insurer offers the consumer a contract, if insurance is competitively provided:

a. any moral hazard or adverse-selection problem is alleviated. b. any moral hazard or adverse-selection problem is worsened. c. the essence of any moral hazard or adverse-selection problem would not change much. d. insurers would no longer offer menus of contracts.

Which of the following is an important implication of the rational expectations argument?

A) Since people form their expectations using all available information, the use of monetary policies to eliminate output gaps will lead to inflation. B) Since any consistent set of monetary policies will be learned and anticipated by a population with rational expectations, policies designed to influence the economy to a level of production other than the potential real GDP will be ineffective. C) Although people may revise their expectations about the price level and future economic activity, they cannot act on these changes because in reality, wages and prices are sticky. Thus, policy intervention is necessary. D) Policymakers must constantly monitor economic activity and revise their economic policy goals to keep up with changing expectations of a population with rational expectations.