8 Guideposts to economic thinking

What will be an ideal response?

1- There is always a tradeoff (opportunity cost)

2- Individuals choose purposefully, therefor economically (highest utility, lowest cost)

3- Incentives matter

4- People make decisions at the margin

5- Information is a costly good

6- Remembering the secondary effects

7- The value of a good or service is subjective

8- The test of a theory is it's ability to predict

You might also like to view...

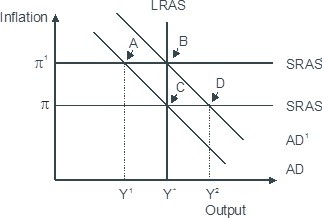

Based on the figure below. Starting from long-run equilibrium at point C, a tax cut that increases aggregate demand from AD to AD1 will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C B. B; C C. B; A D. D; B

A single-price monopoly faces a linear demand curve. If the marginal revenue for the second unit is $20, then the marginal revenue for the

A) first unit is less than $20. B) third unit is less than $20. C) third unit is more than $20. D) third unit is also $20. E) more information is needed to determine if the marginal revenue for the third unit is more than, less than, or equal to $20.

How did the role of government in the East Asian miracle become a factor in the currency crisis of the late 1990s?

What will be an ideal response?

Exhibit 15-6 Dollars per British pound QuantityDemanded Dollarsper Pound QuantitySupplied 200 5 600 240 4 480 300 3 410 360 2 360 390 1 330 In Exhibit 15-6, the equilibrium exchange rate is:

A. 5. B. 4. C. 3. D. 2.