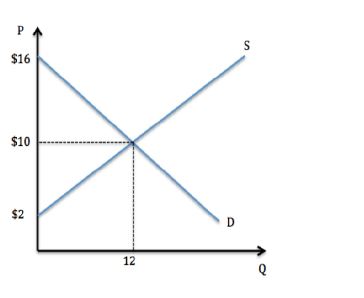

Assume the market was in equilibrium in the graph shown. If the market price gets set to $14, which of the following is true?

A. Some consumers gain surplus, but total surplus falls.

B. Some producers gain surplus, but total surplus falls.

C. Some producers lose surplus, but total surplus rises.

D. Some consumers lose surplus, but total surplus rises.

B. Some producers gain surplus, but total surplus falls.

You might also like to view...

During the housing market and financial crises of 2007 and 2008, the Fed increased the volume of discount loans in an attempt to

A) reassure financial markets and promote financial market stability. B) stabilize prices and reduce the growing inflation rate. C) eliminate structural unemployment to lower the unemployment rate. D) attract foreign investment and stabilize interest rates.

Perfect competition occurs in a market where there are many firms each selling:

A) identical product. B) similar product. C) unique product.

The CPI is a commonly used and closely watched measure of inflation. However, it has limitations. What are they?

What will be an ideal response?

?Which of the following options could be used to eliminate a recessionary gap?

A. Decrease government spending B. ?Decrease consumption C. Decrease investment D. ?Decrease taxes