Give an example that is not in the text of a good that has a change of demand, but not a change of supply. What effect does this change have on the good’s equilibrium price and quantity?

What will be an ideal response?

Should show a thorough understanding of how a change of demand, but not a change in supply, can affect a good’s price and quantity. For example, a celebrity endorsement can significantly increase the demand for a type of blue jeans. However, because production is planned far in advance, the supply may remain the same for some time. As a result, the product is no longer in equilibrium because the quantity demanded is greater than the quantity supplied. As buyers compete for this product, the price increases, which causes the quantity demanded to decrease and the quantity supplied to increase until a new equilibrium is established.

You might also like to view...

Oligopolistic firms tend to make large economic profits over time because

A. they have complete control in the market to charge any price they want. B. they produce at a point that is allocatively efficient. C. they charge higher than average total cost prices. D. they are productively efficient and produce the least costly way.

Consider the table below, in which each production choice represents a point on a production possibility curve.ChoiceEggsRyeA100B810C620D430E240F050This production possibility table could be graphed as a:

A. curved line with negative slope. B. straight line with negative slope. C. straight line with zero slope. D. curved line with positive slope.

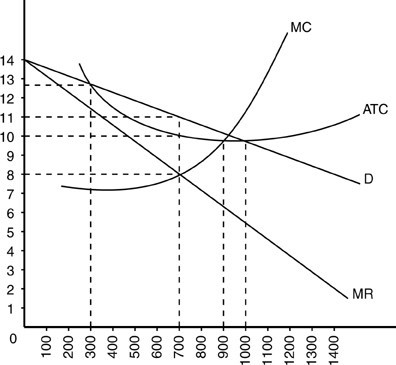

In the above figure, when this monopolistically competitive firm produces its profit-maximizing output, it sets a per-unit price of

In the above figure, when this monopolistically competitive firm produces its profit-maximizing output, it sets a per-unit price of

A. $13. B. $10. C. $8. D. $11.

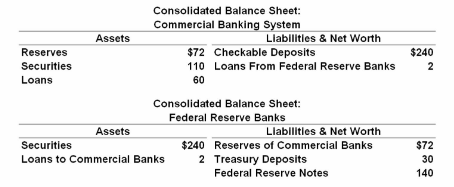

Refer to the given balance sheets. If the reserve ratio is 25 percent, the maximum money- creating potential of the commercial banking system is:

A. $36.

B. $17.

C. $48.

D. $24.