There is a proverb "anything worth doing is worth doing well." Do you think an economist would agree with this proverb?

What will be an ideal response?

Probably not (unless this economist is one of your parents). An economist is likely to tell you that you should follow the Principle of Optimization at the Margin and that you should do something well only if the marginal benefits of doing it well are at least as large as the marginal costs. Suppose you are thinking of painting your room and you have three options: decide not to paint, paint but do a sloppy job, or paint and be meticulously careful. An economist would tell you to paint your room carefully if the marginal benefit of being careful (i.e., the difference between how your room would look if you are careful and how it would look if you are sloppy) is at least as large as the additional cost of painting carefully. Remember that because of scarcity, we cannot have everything we want. Suppose you get 95% of the benefit from painting your room to perfection while doing a sloppy job. The additional 5% in benefits from striving for perfection may well cost more than it is worth, in terms of alternative uses for your time.

You might also like to view...

Marginal product equals

A) the total product produced by a certain amount of labor. B) the change in total product that results from a one-unit increase in the quantity of labor employed. C) total product divided by the quantity of labor. D) the amount of labor needed to produce an increase in production. E) total product minus the quantity of labor.

In the case of externalities, government can use taxes and subsidies to turn an inefficient outcome into an efficient outcome.

Answer the following statement true (T) or false (F)

The most commonly accepted objective for a firm is

A) to stay in business at all cost. B) to maximize total revenue. C) to maximize economic profit. D) to minimize the variable cost outlay.

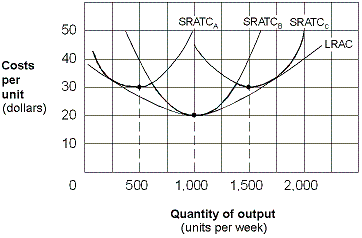

Exhibit 7-15 Long-run average cost In Exhibit 7-15, short-run average total cost, short-run marginal cost, and long-run average cost are all equal at which level of output per week?

In Exhibit 7-15, short-run average total cost, short-run marginal cost, and long-run average cost are all equal at which level of output per week?

A. 500 units. B. 1,000 units. C. 1,500 units. D. 2,000 units.