If an industry's long-run supply curve slopes downward, then the industry is

A) a fixed-cost industry.

B) a constant-cost industry.

C) an increasing-cost industry.

D) a decreasing-cost industry.

D

You might also like to view...

Refer to Figure 4-7. The figure above represents the market for iced tea. Assume that this is a competitive market. If the price of iced tea is $1, what changes in the market would result in an economically efficient output?

A) The price would increase, the quantity supplied would increase, and the quantity demanded would decrease. B) The price would increase, quantity demanded would increase, and quantity supplied would decrease. C) The quantity supplied would increase, the quantity demanded would decrease, and the equilibrium price would increase. D) The price would increase, the demand would increase, and the supply would decrease.

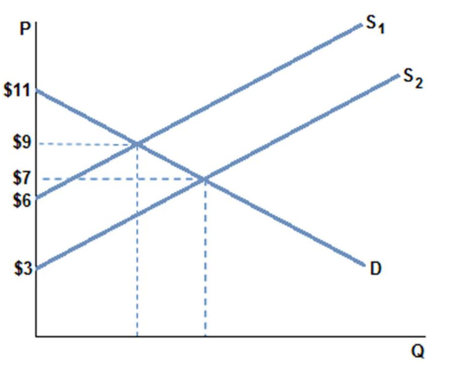

Assume the market in the graph shown with demand D and supply S1 is in equilibrium at a quantity of 5 units. Consumer surplus is:

A. $5.

B. $10.

C. $45.

D. $9.

Which of the following would reduce the supply of computers?

a. higher wage rates for the workers that assemble the computers b. a technological improvement that lowers the cost of producing the computers c. a reduction in the price of computer chips used to produce the computers d. All of the above would reduce the supply of computers.

A production indifference curve shows all combinations of input quantities capable of producing a given quantity of output

a. True b. False Indicate whether the statement is true or false