Average total cost is equal to

A. The sum of average variable cost and marginal cost.

B. Total cost divided by quantity produced.

C. Total cost divided by fixed cost.

D. Total cost multiplied by quantity.

Answer: B

You might also like to view...

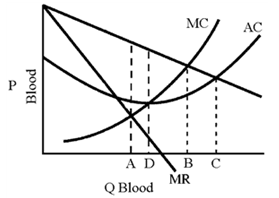

Figure 11-1

The Red Cross is virtually the only operator of blood banks in the United States. In Figure 11-1 are the demand and supply curves facing the Red Cross blood bank. If it were to operate like a profit-maximizing business, how many units of blood would it sell?

The Red Cross is virtually the only operator of blood banks in the United States. In Figure 11-1 are the demand and supply curves facing the Red Cross blood bank. If it were to operate like a profit-maximizing business, how many units of blood would it sell?

A. OA B. OB C. OC D. OD

Marginal revenue is the change in:

a. total revenue resulting from a one unit change in output. b. total revenue resulting from a change in marginal cost. c. price resulting from a one unit change in output. d. none of these.

The long-run industry supply curve will be upward-sloping if:

A. output prices are fixed no matter what the level of output. B. there are no economies or diseconomies of scale. C. input prices are fixed no matter what the level of output. D. input prices increase with the level of output.

An important similarity between a monopolistically competitive firm and a purely competitive firm is that:

A. both face perfectly elastic demand schedules. B. economic profit tends toward zero for both. C. both realize productive efficiency. D. both realize allocative efficiency.