Consumers are most satisfied when

A. all of their income has been saved.

B. the total level of utility is as high as possible.

C. they save more than they spend.

D. goods are bought "on sale."

Answer: B

You might also like to view...

Which of the following firms is the closest to being a perfectly competitive firm?

a. the New York Yankees b. Apple, Inc. c. DeBeers diamond wholesalers d. a wheat farmer in Kansas

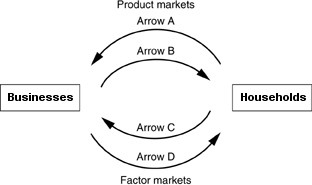

Refer to the above figure. Which arrows represent items that are NOT measured in dollar terms?

Refer to the above figure. Which arrows represent items that are NOT measured in dollar terms?

A. Arrows A and B B. Arrows C and D C. Arrows A and D D. Arrows B and C

If a firm in a perfectly competitive market raises its price

A. it will sell more products. B. it will sell nothing. C. its sales will remain unchanged. D. it will sell fewer products.

Based on the Taylor rule, in the 1980s, monetary policy was

A. just about right. B. too tight. C. too easy. D. too tight in the first half of the decade and too easy in the second half.