Which of the following statements best describe the price, output, and profit conditions of monopoly?

a. Price will equal marginal cost at the profit-maximizing level of output and profits will be positive in the long-run.

b. Price will always equal average variable cost in the short-run and either profits or losses may result in the long run.

c. In the long-run, positive economic profit will be earned.

d. All of these are true.

c

You might also like to view...

Tom is willing to contribute $400 toward building a public park, Jack is willing to contribute $500, and Joe is willing to contribute $750

What is the total marginal value for the park if Tom, Jack, and Joe are the only residents in the neighborhood where the park is being built? A) $1,650 B) $1,050 C) $3,300 D) $2,350

Suppose market demand and supply are given by Qd = 100 - 2P and QS = 5 + 3P. The equilibrium quantity is:

A. 45. B. 62. C. 81. D. 92.

Prices below the free market equilibrium price are inefficient because:

A. producer surplus is lower than in equilibrium. B. consumer surplus is higher than in equilibrium. C. total surplus is lower than in equilibrium. D. total surplus is higher than in equilibrium.

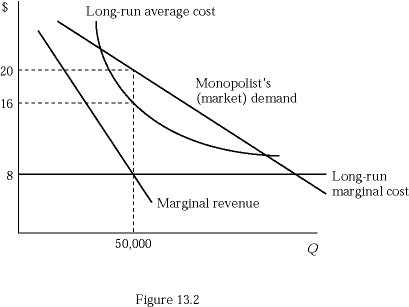

Consider an unregulated monopoly in Figure 13.2. If that monopoly sets its price equal to its marginal cost, it would:

Consider an unregulated monopoly in Figure 13.2. If that monopoly sets its price equal to its marginal cost, it would:

A. earn negative profits. B. earn maximum profits. C. earn zero profits. D. earn small, but greater than zero, profits.