If the supply of a good decreases and demand remains constant equilibrium price:

a. Will decrease, and equilibrium quantity will increase

b. Will increase, and equilibrium quantity will decrease

c. And quantity will decrease

d. And quantity will increase

Answer: b. Will increase, and equilibrium quantity will decrease

You might also like to view...

A deadweight loss of consumer and/or producer surplus occurs when:

a. producers fail to maximize profits. b. mutually beneficial transactions cannot be completed. c. consumers do not maximize their utility. d. the price of inputs increases.

The economy is in equilibrium, TP = TE, and Real GDP is $4,555 billion. The MPC is 0.80, the multiplier is operative, and idle resources exist at each expenditure round. Government purchases rise by $10 billion. As a result, the __________ curve shifts __________, inventory levels unexpectedly __________, business firms ___________ the quantity of goods and services they produce, and Real GDP

__________ by __________. A) TE; downward; fall; increase; rises; $10 billion. B) TP; rightward; fall; decrease; falls; $50 billion C) TE; upward; fall; increase; rises; $50 billion D) TE; downward; rise; increase; rises, $50 billion

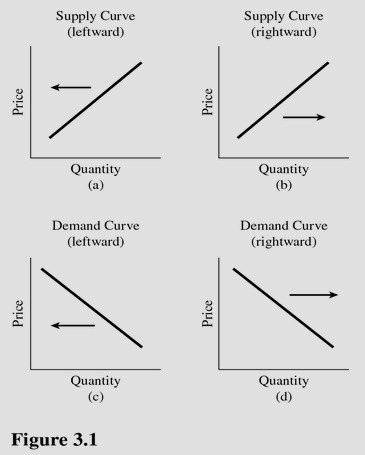

Choose the letter of the diagram in Figure 3.1 that best describes the type of shift that would occur in each situation for the market listed on the left, ceteris paribus. Figure 3.1 Shifts of Supply and Demand for Flat-screen TVs: the technology required for flat-screen TV production becomes cheaper.

A. A. B. B. C. C. D. D.

If a hurricane were to wipe out the majority of the eastern seaboard in the United States, it would likely cause a:

A. short-run supply shock. B. long-run supply shock. C. long-run demand shock. D. short-run demand shock.