Because marginal cost is always ________ in the short run, total variable cost always ________ when output decreases.

A. positive; increases

B. negative; increases

C. negative; decreases

D. positive; decreases

Answer: D

You might also like to view...

Available market incentives for clean fuel vehicles

a. include carbon allowances for purchasers of hybrid vehicles b. no longer exist in the United States c. are tax credits for purchasers of plug-in hybrids d are limited to international buyers of electric cars

A demand curve is described as perfectly inelastic if

A. the same quantity is purchased regardless of price. B. the same price is charged regardless of quantity sold. C. neither price nor quantity demanded ever change. D. only quantity demanded can change.

The difference between the existing unemployment rate and the natural unemployment rate is defined is the __________ unemployment rate.

a. frictional b. structural c. cyclical d. natural

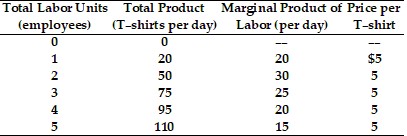

Refer to the data provided in Table 10.1 below to answer the following question(s).

Table 10.1  Refer to Table 10.1. The marginal revenue product of the fourth worker is

Refer to Table 10.1. The marginal revenue product of the fourth worker is

A. $5. B. $20. C. $100. D. $475.