In a perfectly competitive industry,

a. the market price is determined at the intersection of the market supply and demand curves

b. the typical firm will just break even in the short run

c. a rise in the market price will attract new entrants

d. economics profits are a signal for new consumers to enter

e. each firm faces the downward sloping market demand curve

A

You might also like to view...

A market in which there is only one seller, and there is no close substitute for the product being sold, is called

A) perfect competition. B) monopolistic competition. C) monopoly. D) oligopoly.

Marginal resource cost is the

a. cost of hiring another unit of a resource b. additional revenue generated by hiring one more unit of a resource c. additional output generated by hiring one more unit of a resource d. total cost of hiring a resource e. average cost of hiring a resource

An example of deflation since the base year would be a CPI in the current year of

A. 90. B. 100. C. 110. D. 200.

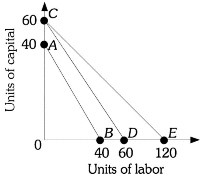

Refer to the information provided in Figure 7.9 below to answer the question(s) that follow.  Figure 7.9Refer to Figure 7.9. The firm's isocost line could shift from AB to CD if

Figure 7.9Refer to Figure 7.9. The firm's isocost line could shift from AB to CD if

A. the price of capital decreased. B. the firm's total expenditures increased by 50%. C. the price of capital and labor each decreased by 33.3%. D. either B or C