Which of the following is true, if real GDP in Year 1 is €5,000 and in Year 2 is €5,200?

(a) Output has increased by 4 percent.

(b) Output has declined by 4 percent.

(c) Output change is uncertain.

(d) The economy is experiencing 4 percent inflation.

Answer: (a) Output has increased by 4 percent.

You might also like to view...

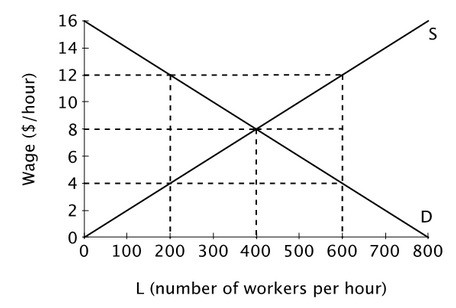

Consider the accompanying figure representing the labor market below. If a minimum wage of $12 per hour is imposed in this labor market then worker surplus will ________ and employer surplus will ________.

If a minimum wage of $12 per hour is imposed in this labor market then worker surplus will ________ and employer surplus will ________.

A. stay the same; fall B. fall; fall C. rise; fall D. rise; stay the same

Suppose that the price of macaroni drops. Quantity supplied will ________ and producer surplus will ________.

A. increase; increase B. increase; decrease C. decrease; increase D. decrease; decrease

When marginal product is rising

A) total product is falling. B) marginal cost is falling. C) marginal cost is rising. D) average fixed cost is rising.

When money serves as a store of value, it allows you to

A. transfer wealth into the future. B. be an effective negotiator. C. find good bargains. D. eliminate a double coincidence of wants.