The second fundamental theorem of welfare economics states that

A) under certain conditions, a competitive equilibrium is Pareto optimal.

B) a competitive equilibrium is always Pareto optimal.

C) under certain conditions, a Pareto optimum is a competitive equilibrium.

D) a Pareto optimum is always a competitive equilibrium.

C

You might also like to view...

Miniville is an isolated town located on the southern shore of Lake Condescending, a very large lake. The western edge of Miniville is adjacent to impassable mountains and there are no towns or businesses for many miles to the east. The 300 residents of Miniville are evenly distributed along 3 miles of shoreline on the lake, east of the mountains. Lake Shore Drive, the only street in town, provides access to Miniville's homes and businesses. All residents live between the lake and the street; businesses locate on the other side of the street. Lake Shore Drive is 3 miles long, and the points labeled A, B, and C are 1, 2, and 3 miles from the western end of Lake Shore Drive, respectively. All residents of Miniville shop at the store located closest to their homes. src="https://sciemce.com/media/4/ppg__rrr0818190951__f1q364g1.jpg" alt="" style="vertical-align: 0.0px;" height="117" width="538" />If three stores were to open sequentially, you would expect that those stores would be located:

A. in a cluster, nearest the mountains.

B. at points A, B, and C.

C. in a cluster, near the location chosen by the first store to locate.

D. halfway between the mountains and A, halfway between A and B, and halfway between B and C.

Total factor productivity is

a. changes in amounts of factors of production b. changes in output due to changes in the amount of factors of production c. changes in output due to changes in productivity of factors of production d. changes in productivity of factors of production due to changes in other factors e. none of the above

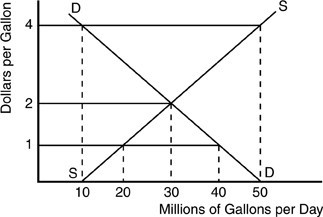

According to the above figure for a gasoline market, at a price of $1 per gallon of gasoline, there would be

According to the above figure for a gasoline market, at a price of $1 per gallon of gasoline, there would be

A. a surplus of 50 million gallons. B. a shortage of 30 million gallons. C. a surplus of 30 million gallons. D. a shortage of 20 million gallons.

The price of crude oil increased to $100 per barrel in early 2008. What would we expect to see happen to the supply of gasoline, which is produced using crude oil?

A) The supply of gasoline will increase. B) The supply of gasoline will decrease. C) The supply of gasoline will stay the same because the government requires gasoline producers to meet statutory minimum production levels. D) The supply of gasoline will stay the same because of the profit motives of gasoline producers.