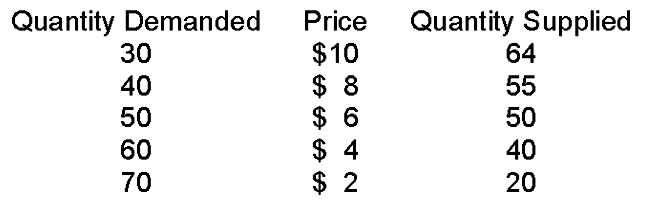

When the price is $2

A. quantity supplied is greater than quantity demanded and, therefore, price must rise to get to equilibrium.

B. quantity supplied is less than quantity demanded and, therefore, price must fall to get to equilibrium.

C. quantity demanded is greater than quantity supplied and, therefore, price must rise to get to equilibrium.

D. quantity demanded is greater than quantity supplied and, therefore, price must fall to get to equilibrium.

C. quantity demanded is greater than quantity supplied and, therefore, price must rise to get to equilibrium.

You might also like to view...

Necessities, such as food and shelter, are product purchases that consumers are sensitive to, so the demand is elastic for these goods.

Answer the following statement true (T) or false (F)

Intermediate goods and services are:

A. used only as inputs to produce something else and are not counted as separate items in GDP. B. goods that consumers buy in parts-like a new tire for their car-and are included as separate items in GDP. C. used only as inputs to produce something else and are counted as separate itemsin GDP. D. goods that consumers buy in parts-like a new tire for their car-and are not included as separate items in GDP.

In February 2015, the unemployment rate for those with a college degree was __________.

a. 2.7% b. 5.1% c. 5.4% d. 8.4%

Which of the following is an exogenous variable in the Three-Sector-Model?

a. Oil prices b. Real GDP c. Quantity of real credit per time period d. Quantity of currency per time period e. All of the above are exogenous variables.