As of the year 2000, manufacturing, mining, and construction accounted for what percentage of total U.S. output?

A. 19 percent.

B. 15 percent.

C. 28 percent.

D. None of the choices are correct.

Answer: A

You might also like to view...

Monopolistic competitors in long-run equilibrium will generally find that they are earning economic profits

a. True b. False Indicate whether the statement is true or false

For firms that sell one product in a perfectly competitive market, the market price:

A. is equal to the average total cost of a firm. B. is higher than the marginal revenue of a firm C. can be influenced by one firm's output decision. D. is taken as a constant by individual firms.

At the equilibrium price, the quantity of the good that buyers are willing and able to buy

a. is greater than the quantity that sellers are willing and able to sell. b. exactly equals the quantity that sellers are willing and able to sell. c. is less than the quantity that sellers are willing and able to sell. d. Either a) or c) could be correct.

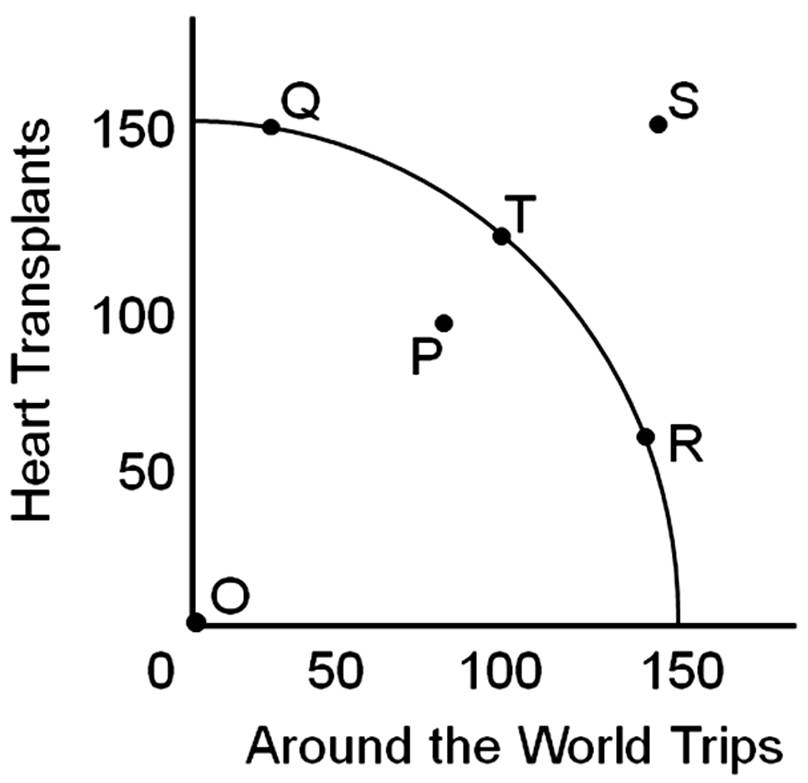

The opportunity cost of moving from point T to point Q would be

A. giving up trips around the world.

B. giving up heart transplants.

C. gaining trips around the world.

D. gaining heart transplants.