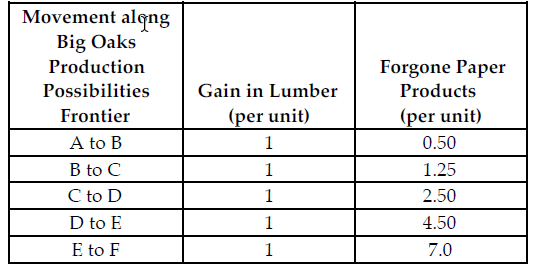

Refer to the table below. If the profit for each unit of paper product is $3.00 and the profit for each unit of lumber is $13.50, what is the marginal benefit for each unit of lumber produced?

Big Oaks can produce either paper products or lumber with each tree that they harvest. Because Big Oaks can adjust the amount of paper products and lumber they produce from the harvested trees, paper products and lumber are produced in variable proportions. The above table summarizes Big Oaks production possibilities from each harvested tree.

A) $13.50

B) $16.50

C) $10.50

D) $3.00

A) $13.50

You might also like to view...

Which of the following is true?

i. When the world price of a good is lower than the price that balances domestic supply and demand, a country gains from exporting the good. ii. Compared to a no-trade situation, in a market with imports, consumer surplus is larger. iii. Quotas raise the domestic price of imported goods. A) only i B) only ii C) only iii D) i and ii E) ii and iii

If trade opens up between the two formerly autarkic countries, Australia and Belgium, then

A) the real income of both countries may increase. B) the real income of Australia and of Belgium will increase. C) the real income of Australia but not of Belgium will increase. D) the real income of neither country will increase. E) the real income of both countries will increase.

Many state and local governments find themselves faced with increasing retirement expenditures for retired government employees. These increasing expenditures will ________ GDP because they are categorized as ________

A) increase; government purchases B) increase; gross private domestic investment C) decrease; state and local government purchases D) not change; transfer payments.

Which of the following statements is true? a. Demand refers to how much of a good a consumer is willing to purchase at all prices

b. Demand refers to how much of a good a consumer is able to purchase at all prices. c. Demand refers to how much of a good a consumer is able to consume during a given period of time. d. Demand refers to how much of a good a consumer is willing and able to purchase at all prices.