The existence of positive economic profits in an industry attracts new entrants into the industry.

Answer the following statement true (T) or false (F)

True

In the long run, firms will enter an industry as long as they can earn a greater than normal (zero) profit.

You might also like to view...

The graph illustrates the market for bottled water. When the price exceeds the equilibrium price, the quantity demanded is ________ the quantity supplied and the price of the good will ________

A) less then; fall B) greater than; fall C) equal to; fall D) less than; rise E) greater than; rise

The marginal revenue of a price taker is:

a. equal to price. b. less than price. c. more than price. d. unrelated to price.

Health care improvements often don't happen because:

A. they are too expensive to implement. B. doctors overprescribe and drive the cost of health care too high. C. health care facilities don't exist in some parts of the world. D. they are too expensive to have any significant impact.

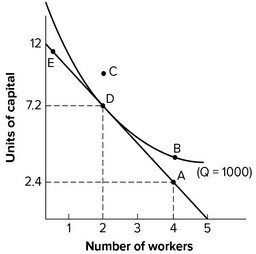

Refer to the graph shown. The cheapest way to produce 1,000 units of output is with:

A. 4 workers and 2.4 units of capital. B. 12 units of capital and no workers. C. 5 workers and no capital. D. 2 workers and 7.2 units of capital.