In a perfectly competitive market:

A) the long-run market price is equal to the average fixed cost of the industry.

B) the long-run market price is less than the minimum average cost of the industry.

C) the long-run market price is more than the minimum average cost of the industry because of free entry and exit of firms.

D) the long-run market price is equal to the minimum average cost of the industry because of free entry and exit of firms.

D

You might also like to view...

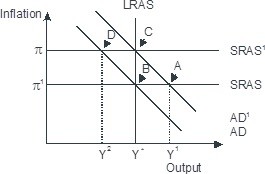

Based on the figure below. Starting from long-run equilibrium at point C, a tax increase that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C B. D; B C. A; B D. B; C

Suppose in the market for labor that the labor supply curve is perfectly inelastic. This would mean that the supply curve is vertical. Furthermore, suppose that demand is normal and downward sloping. Your textbook has explained that unemployment taxes are paid entirely by the employer (demanders). Who actually pays the tax in the scenario described above?

What will be an ideal response?

Refer to Scenario 15.5. If Catherine stopped smoking, then what is the total amount that Catherine will save on life insurance premiums over the rest of her expected lifespan?

A) $700 B) $14,000 C) $30,000 D) $42,000 E) $56,000

In which year did long-term interest rates in Greece rise to an all-time high of close to 30%?

A. 2003 B. 2011 C. 2009 D. 2005