Which of the following, necessarily, equals zero when the firm's short-run output level is zero?

a. sunk costs

b. fixed costs

c. implicit costs

d. variable costs

e. opportunity costs

D

You might also like to view...

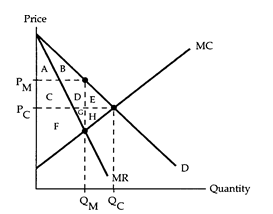

Refer to the market diagram. Relative to the surplus achieved under perfect competition, how much surplus is lost (deadweight loss) when there is a monopoly?

The following questions refer to the accompanying market diagram. PC and QC are the equilibrium price and quantity if the firm behaves competitively, and PM and QM are the equilibrium price and quantity if the firm is a simple monopoly.

a. E

b. H

c. E + H

d. D + G + E + H

The policy that aims to regulate and prevent anti-competitive pricing in the United States is referred to as:

A) antitrust policy. B) anticompetition policy. C) monopoly regulation policy. D) consumer protection policy.

We are using resources efficiently if we can produce more of one good without producing less of some other good that we value more highly

Indicate whether the statement is true or false

How can crime and punishment be modeled as a principal-agent problem? What does the model suggest about crime prevention?

What will be an ideal response?