Under what circumstances will the equilibrium in a trust game be efficient?

What will be an ideal response?

In a trust game, the first mover has to decide whether he will trust the second mover or not. If he chooses to trust the second mover, the second mover can either cooperate or defect. If he cooperates, both the players will earn a higher payoff than they would have if the first player chose not to trust. If the second mover defects, he will earn a higher payoff than the first player. Therefore, the second mover always has an incentive to defect. Given that the second mover is likely to defect, the first mover chooses not to trust. This results in a socially inefficient equilibrium. However, if the second mover has a reputation of trustworthiness, the first mover will choose to trust him and both of them will earn a higher payoff leading to an efficient outcome. Such an efficient outcome can also occur if the game is repeated several times because the players will then realize that they can maximize their payoffs if the first mover chooses to trust and the second mover chooses to cooperate.

You might also like to view...

The circular flow of income shows that GDP can be measured as the sum of wages, interest, rent, and profits received by households or total expenditures on goods and services by households, firms, government, and the rest of the world

Indicate whether the statement is true or false

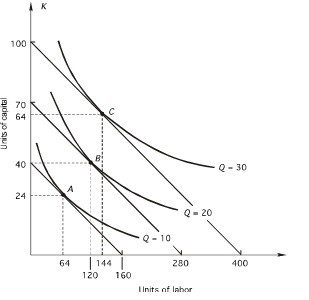

In the following graph, the price of capital is $100 per unit; the price of labor is $25 per unit. How much does the seventh unit of output add to total cost?

A. nothing B. $400 C. $800 D. $4,000 E. $8,000

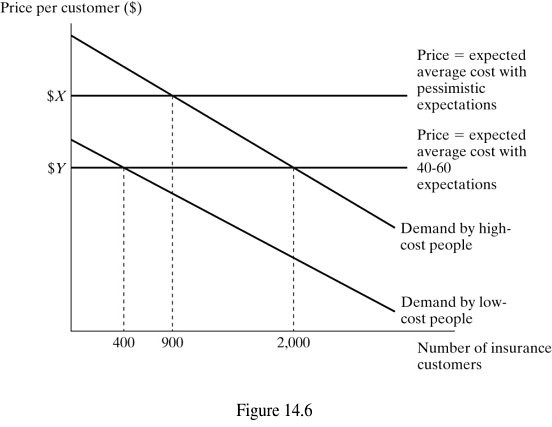

Figure 14.6 represents the market for health insurance. Suppose there are two types of consumers, low-cost consumers with $2,000 average medical expenses per year, and high-cost customers with $4,000 average medical expenses per year. The insurance companies estimate that 40% of its customers are high-cost type. The uninformed side(s) of the market is (are):

Figure 14.6 represents the market for health insurance. Suppose there are two types of consumers, low-cost consumers with $2,000 average medical expenses per year, and high-cost customers with $4,000 average medical expenses per year. The insurance companies estimate that 40% of its customers are high-cost type. The uninformed side(s) of the market is (are):

A. customers. B. insurance companies. C. both customers and insurance companies. D. neither customers nor insurance companies.

In which market model would there be a unique product for which there are no close substitutes?

A. Monopolistic competition B. Pure competition C. Pure monopoly D. Oligopoly