In a long-run monopolistically competitive equilibrium

A. P > ATC, and ATC is not at its minimum value.

B. P = ATC, and ATC is not at its minimum value.

C. P > ATC, and ATC is at its minimum value.

D. P = ATC, and ATC is at its minimum value.

Answer: B

You might also like to view...

Oil refiners can refine a barrel of petroleum so that it yields either more home heating oil or more diesel fuel. If the price of diesel fuel falls, there is

A) an increase in the supply of home heating oil. B) a decrease in the supply of home heating oil. C) an increase in the quantity of home heating oil supplied. D) a decrease in the quantity of home heating oil supplied. E) an increase in the demand for home heating oil.

What is the difference between the Current Population Survey and the establishment survey? What are the major drawbacks for each of these measures of unemployment?

What will be an ideal response?

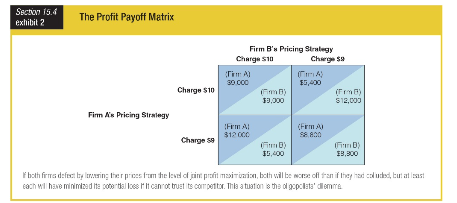

Which condition is the Nash equilibrium for this scenario?

a. Each firm charges $9.

b. Each firm charges $10.

c. Firm A charges $10 while Firm B charges $9.

d. Firm B charges $10 while Firm A charges $9.

Why do increasing returns to scale in an industry make it more likely that the industry will be oligopolistic rather than perfectly competitive?

What will be an ideal response?