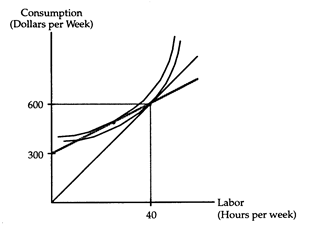

Mary is a waitress who, when tips are included, earns $15 per hour. Mary chooses to work 40 hours per week. Assume there are no taxes, so Mary earns $600 per week. A slowdown in the restaurant's business cuts Mary's hourly wage in half, to $7.50 per hour. To compensate Mary for the lost income, Mary's rich parents begin sending a gift of $300 per week.

(i) Design an indifference curve-budget line diagram illustrating this situation.

(ii) Does Mary now choose to work more or fewer hours? Does Mary's consumption rise, fall, or remain unchanged? Is Mary now better off or worse off?

(i) If Mary chooses to work 40 hours per week, total earning will continue to equal $600 per week ($300 per week in wages plus the $300 per week gift). Thus Mary's new budget line passes through the initial optimum as shown below.

(ii) Mary chooses to work fewer hours, because the lower relative wage creates a substitution effect. Mary will now earn less than $300 in labor income, so Mary's consumption will fall. Mary is better off because the gift is large enough to place the new optimum on a higher indifference curve.

You might also like to view...

Suppose the economy's production function is Y = AK0.3N0.7. When K = 1000, N = 50, and A = 15, what is Y?

A) 1842 B) 6106 C) 750,000 D) 123

Which of the following is true of exchange?

a. Exchange is a zero sum activity; if one party to an exchange gains, the other must lose an equal amount. b. The exchange value of a good is determined by the cost of the resources required to produce the good. c. The total output trading partners are able to produce is not influenced by whether the partners trade with each other. d. Exchange permits trading partners to expand their total output of goods and services as the result of greater specialization in areas where each has a comparative advantage.

The legislation which prohibited selling products at unreasonably low prices was the:

A. Sherman Act. B. Clayton Act. C. Robinson-Patman Act. D. Celler-Kefauver Act.

Marginal revenue is

A) total revenue divided by the total quantity of output. B) the change in profit divided by the change in the quantity of output. C) the change in total revenue divided by the change in total cost. D) the change in total revenue divided by the change in the quantity of output.