Which of the following statements best describes the price, output, and profit conditions of monopolistic competition?

A. Price will equal marginal cost at the profit-maximizing level of output; profits will be positive in the long-run.

B. Price will always equal average variable cost in the short run and either profits or losses may result in the long run.

C. Marginal revenue will equal marginal cost at the short run, profit-maximizing level of output; in the long run, economic profit will be zero.

D. Marginal revenue will equal average total cost in the short run; long-run economic profits will be zero.

Answer: C

You might also like to view...

In 2008, the Fed responded to the financial crisis by:

A. offering nearly unlimited short-term financing to any bank that suddenly found itself short on cash. B. increasing the interest rates to encourage people to save, so banks would have more money on hand to lend. C. doing nothing, and allowing the automatic stabilizers to bring the economy back to its long run equilibrium. D. reducing money supply.

Sales taxes generate nearly 50% of the tax revenue for state and local governments

a. True b. False Indicate whether the statement is true or false

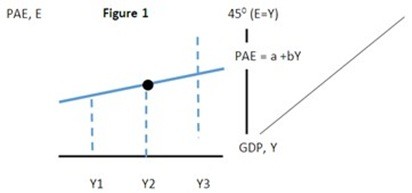

In Figure 1 above the Keynesian equilibrium occurs at what output level?

In Figure 1 above the Keynesian equilibrium occurs at what output level?

A. Y2 B. Y3 C. Y1 D. it does not occur at any output level in the graph.

According to "Oil Spikes On OPEC Pact," OPEC wants to behave like a monopoly, choosing a rate of industry output that maximizes total industry profit. The challenges for all cartels, OPEC in particular, include all of the following except

A. Replicating monopoly outcomes. B. Coordination. C. Allocating market share. D. Preventing some members from decreasing production.