An economy in which government bureaucracy decides how much of a good to produce, how to produce the good, and who gets the good is known as a

A) centrally planned economy. B) market economy.

C) mixed economy. D) laissez-faire economy.

A

You might also like to view...

A rising average cost implies that

a. marginal cost is equal to average cost b. marginal cost is above average cost c. marginal cost is below average cost d. none of the above

The perfectly competitive firm's supply curve includes

a. that portion of the marginal cost curve above the minimum point on the average variable cost curve b. its economic profit schedule c. that portion of the marginal revenue curve above minimum average variable cost d. that portion of the average total cost curve above minimum average variable cost e. the firm's effective resource demand curve

An extreme case in which a percentage change in price, no matter how large, results in zero change in quantity is called:

a. perfect inelasticity. b. perfect elasticity. c. strong elasticity. d. weak elasticity.

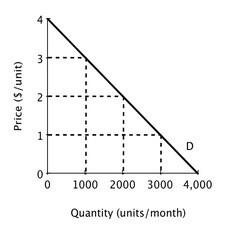

Quick Buck and Pushy Sales produce and sell identical products and face zero marginal and average cost. Below is the market demand curve for their product. Suppose Quick Buck and Pushy Sales decide to collude and work together as a monopolist with each firm producing half the quantity demanded by the market at the monopoly price. If Quick Buck cheats by reducing its price to $1 while Pushy Sales continues to comply with the collusive agreement, then Quick Buck's economic profit will be ________.

Suppose Quick Buck and Pushy Sales decide to collude and work together as a monopolist with each firm producing half the quantity demanded by the market at the monopoly price. If Quick Buck cheats by reducing its price to $1 while Pushy Sales continues to comply with the collusive agreement, then Quick Buck's economic profit will be ________.

A. $4,000 B. $3,000 C. $2,000 D. $6,000