What is the difference between between total costs, variable costs, and fixed costs?

What will be an ideal response?

Total costs are the costs of all inputs a firm uses in production. Variable costs are costs that change as output changes. Fixed costs are costs that remain constant as output changes. Total cost is equal to the sum of variable costs and fixed costs.

You might also like to view...

The amount of interest owed on a loan of $100,000 after a year at an interest rate of 3 percent is:

A. $3,000. B. $30,000. C. $103,000. D. $100,300.

The government wishes to close an inflationary gap by reducing national income by $400 billion. Assuming a tax multiplier of 4 and an income multiplier of 5, which of the following policy prescriptions would reduce the inflationary gap by $400 billion?

a. decreasing government spending by $400 billion and increasing taxes by $400 billion b. decreasing government spending by $160 billion and decreasing taxes by $100 billion c. decreasing government spending by $40 billion and decreasing taxes by $40 billion d. decreasing government spending by $80 billion and keeping taxes the same e. doing absolutely nothing to the economy

A reduction in the level of unemployment would have which effect with respect to the nation's production possibilities curve?

A. It would shift the curve to the left. B. It would shift the curve to the right. C. It would not shift the curve; it would be represented by moving from a point inside the curve toward the curve. D. It would not shift the curve; it would be represented by moving from a point on the curve to a point outside the curve.

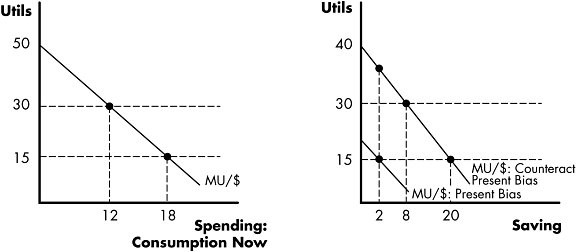

Figure 7.5 The consumer must decide how to split $20 between spending and saving.Refer to Figure 7.5. If the consumer uses cognition to offset present bias, he/she will consume ________ now and save ________ to maximize utility.

The consumer must decide how to split $20 between spending and saving.Refer to Figure 7.5. If the consumer uses cognition to offset present bias, he/she will consume ________ now and save ________ to maximize utility.

A. $12; $8 B. $18; $2 C. $12; $2 D. $0; $20