In an increasing-cost industry, an increase in industry output will

A. shift each firm's short run supply curve down.

B. shift each firm's average fixed cost curve down.

C. lead to a lower market price.

D. lead to a higher market price.

Answer: D

You might also like to view...

Which of the following is not a characteristic of a perfectly competitive market structure?

A) There are restrictions on exit of firms. B) There are no restrictions to entry by new firms. C) There are a very large number of firms that are small compared to the market. D) All firms sell identical products.

A monopolistically competitive firm earning profits in the short run will find the demand for its product decreasing and becoming more elastic in the long run as new firms move into the industry until

A) the original firm is driven into bankruptcy. B) the firm's demand curve is perfectly elastic. C) the firm exits the market. D) the firm's demand curve is tangent to its average total cost curve.

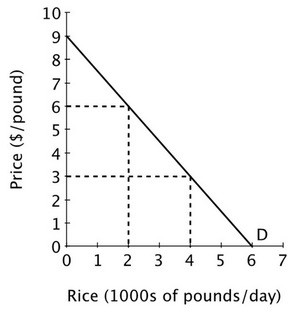

Refer to the accompanying figure. What is the price elasticity of demand when the price of rice is $6 per pound?

A. 2 B. 0.5 C. 3 D. 0.67

Define the following terms and explain their importance to the study of macroeconomics: a. Aggregation b. Recession c. Gross domestic product d. Final goods and services e. Stabilization policy

What will be an ideal response?