Average total cost:

A. decreases when output levels are low, then increases as output increases.

B. increases when output levels are low, then decreases as output decreases.

C. is minimized when it equals average variable cost.

D. is maximized when it equals marginal cost.

A. decreases when output levels are low, then increases as output increases.

You might also like to view...

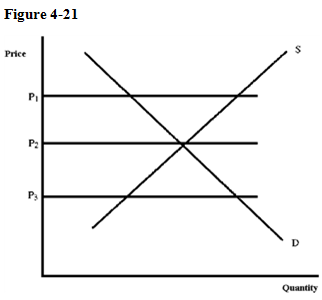

Which price in Figure 4-21 is equilibrium?

Which price in Figure 4-21 is equilibrium?

A. P1 B. P2 C. P3 D. There is no equilibrium price in the diagram.

Betty and Ann live on a desert island. With a day's labor, Ann can produce 8 fish or 4 coconuts; Betty can produce 6 fish or 2 coconuts

Ann's opportunity cost of producing 1 coconut is ________ and she should specialize in the production of ________. A) 8 fish per coconut; fish B) 2 fish per coconut; coconuts C) 6 fish per coconut; coconuts D) 0 fish per coconut; coconuts

If the costs of negotiating and enforcing contracts are high relative to the benefits, buyers and sellers will have incentives to make economically efficient arrangements that increase value

Indicate whether the statement is true or false

A consumer will consume the combination of goods at the crossing point of a budget line and indifference curve

a. True b. False Indicate whether the statement is true or false