In both monopolistically competitive and perfectly competitive industries

A) firms produce products for which there are no close substitutes.

B) there are high barriers to entry.

C) there are many buyers and sellers.

D) firms are price takers.

Answer: C

You might also like to view...

Which of the following demonstrates the law of supply?

a. When the price of leather belts rose, leather belt sellers increase their quantity supplied of leather belts. b. When car production technology improved, car producers increased their supply of cars. c. When sweater producers expected sweater prices to rise in the near future, they decreased their current supply of sweaters. d. When ketchup prices rose, ketchup sellers decreased their quantity supplied of ketchup.

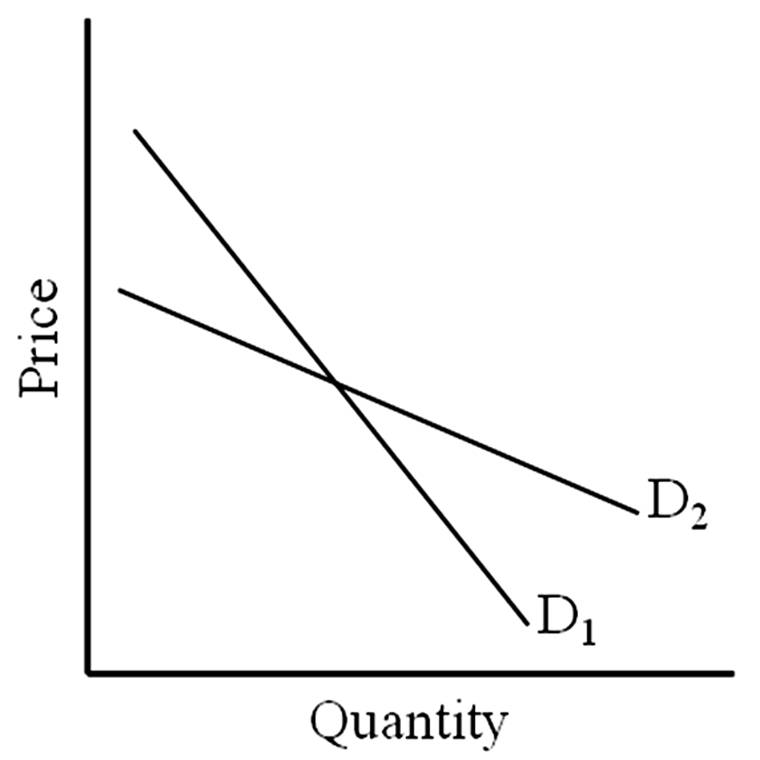

Which statement is true?

A. D1 is more elastic than D2.

B. D2 is more elastic than D1.

C. D1 and D2 have the same elasticity.

D. There is no way to determine the relative elasticities of D1 and D2.

Some economists suggest that because of the costs of negotiating contracts, printing price lists, etc., it is costly for firms to change prices in response to demand changes. This hypothesis is known as the

A. rational expectations theory. B. sticky wage theory. C. menu cost theory. D. Phillips theory.

Quantity Decision

What will be an ideal response?