Using equations for public and private saving, show that saving must equal investment in a closed economy. Begin with the expression for total saving in the economy

What will be an ideal response?

Start with the expression of total saving in the economy. This is the sum of private saving and public saving:

S = Sprivate + Spublic (1 )

where private saving is:

Sprivate = Y + TR - C - T. (2 )

This states that private saving is what is left over from household income after consumption expenditures (C) and taxes (T) are subtracted and transfers (TR) are added.

Public saving is:

Spublic = T - G- TR. (3 )

Public saving is what is left over after government spending (G) and transfer payments (TR) are subtracted from taxes (T).

Combining (2 ) and (3 ) into (1 ) we get

S = Y + TR - C - T + T - G- TR. Note that taxes and transfers cancel each other out leaving:

S = Y - C - G. (4 )

Because we know that income (Y) is exactly equal to production or

Y = C + I + G in a closed economy, we can substitute the right hand side of this expression into

(4), and we get S = C + I + G - C - G. The consumption values cancel as does the level of government spending, leaving S = I.

You might also like to view...

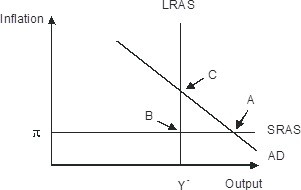

The economy pictured in the figure has a(n) ________ gap with a short-run equilibrium combination of inflation and output indicated by point ________.

A. recessionary; A B. recessionary; C C. recessionary; B D. expansionary; A

During the 20th century, the highest savings rates in the U.S. were observed during

A) the Great Depression. B) World War II. C) the late 1980s and 1990s. D) none of the above.

Economic profits and losses are true market signals because they

A) convey information in an asymmetrical fashion. B) convey information about rewards people should anticipate experiencing by shifting resources from one activity to another. C) convey information to public officials about where to encourage people to invest and what skills people should develop. D) cause people to move into careers in both undesirable and desirable industries with equal ease.

Along a linear demand curve, as the price rises, demand becomes more

a. steep b. elastic c. inelastic d. unit elastic e. variable