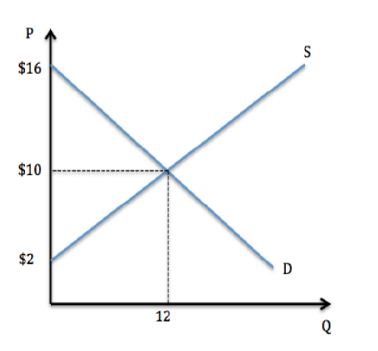

Assume the market was in equilibrium in the graph shown. If the market price gets set to $7, which of the following is true?

A. Some producers gain surplus, but total surplus falls.

B. Some producers lose surplus, but total surplus rises.

C. Some consumers gain surplus, but total surplus falls.

D. Some consumers lose surplus, but total surplus rises.

C. Some consumers gain surplus, but total surplus falls.

You might also like to view...

A firm’s fixed cost

A. does not vary with output. B. does not change between the short run and the long run. C. is generally a higher percentage of its total cost at high output quantities than at low output quantities. D. All of the above are true.

In the case study discussed in the chapter, the electronics firm was losing money by selling its calculators at a price that was below average cost.

Answer the following statement true (T) or false (F)

The artist Pablo Picasso sketched a woman tourist and charged her a lot for just a few minutes work. By his response, this is an example of:

a. Overcharging b. Getting paid for one's life experience, expertise c. Agreement on the woman's part about "fair value" d. Material resources

What happens to a market in equilibrium when there is an increase in supply?

a) excess supply means that producers will make less of the good b) quantity demanded will exceed quantity supplied, so the price will drop c) quantity supplied will exceed quantity demanded, so the price will drop d) undersupply means that the good will become very expensive