Answer the following questions true (T) or false (F)

1. In a decreasing-cost industry, the entry of new firms lowers average cost at each level of output.

2. When firms exit a perfectly competitive industry, the market supply curve shifts to the left.

3. Assume that the personal computer industry is perfectly competitive. The fact that the price of personal computers over the last decade has fallen despite increases in demand signifies that the industry is a decreasing-cost industry.

1. TRUE

2. TRUE

3. TRUE

You might also like to view...

A decision made by a rational person

A) is intended to make the person worse off. B) would always make the person wealthier. C) is identical to a decision that would be made by any other person facing the same choices. D) is intended to make the person better off.

Assume that a college student spends her income on books and pizza. The price of a pizza is $8, and the price of a book is $15 . If she has $120 in income, she could choose to consume

a. 8 pizzas and 4 books. b. 4 pizzas and 6 books. c. 5 pizzas and 5 books. d. 2 pizzas and 7 books.

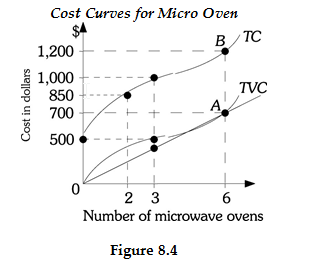

Refer to Figure 8.4. If two microwave ovens are produced, Micro Oven's total variable costs are A) $350. B) $425. C) $500.

Suppose the Fed conducts an open market purchase of bonds. This monetary policy action will tend to cause

A. the price of bonds to decrease, and the interest rate to increase. B. the price of bonds to increase, and the interest rate to increase. C. the price of bonds to decrease, and the interest rate to decrease. D. the price of bonds to increase, and the interest rate to decrease.