At the point where the demand and supply curves for a product intersect:

A. the selling price and the buying price need not be equal.

B. the market may, or may not, be in equilibrium.

C. either a shortage or a surplus of the product might exist, depending on the degree of

competition.

D. the quantity that consumers want to purchase and the amount producers choose to sell are

the same.

Answer: D

You might also like to view...

The highest valued alternative that must be given up to engage in an activity is the definition of

A) marginal cost. B) marginal benefit. C) opportunity cost. D) economic equity.

A small business owner earns $50,000 in revenue annually. The explicit annual costs equal $30,000. The owner could work for someone else and earn $25,000 annually. The owner's business profit is ________ and the economic profit is ________

A) $20,000, $20,000 B) $20,000, -$5,000 C) $25,000, -$5,000 D) $25,000, $20,000

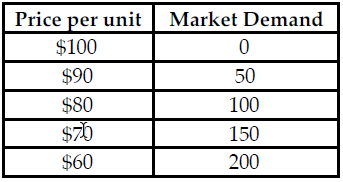

Refer to the table below. If this market is a Cournot Oligopoly and Firm X is produces 50 units, what is Firm Y's demand at a price of $60?

The table above shows the market demand for a product that both Firm X and Firm Y manufacture. Both firms produce an identical product and the firms' average total and marginal cost are equal and constant.

A) 150 B) 100 C) 200 D) 50

Which of the following goods is least likely to be in a market basket?

A. Helicopter B. Gasoline C. Barbie dolls D. Breakfast cereal