When a purely competitive firm is in long-run equilibrium, price is equal to:

A. marginal cost, but may be greater or less than average cost.

B. marginal revenue but may be greater or less than both average and marginal cost.

C. minimum average cost but may be greater or less than marginal cost.

D. minimum average cost and also to marginal cost.

Answer: D

You might also like to view...

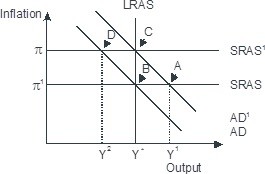

Based on the figure below. Starting from long-run equilibrium at point C, a tax increase that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C B. D; B C. A; B D. B; C

If the Fed makes the quantity of money grow at the same rate as the growth rate of real GDP and velocity does not change, in the long run what happens to the price level and the inflation rate?

What will be an ideal response?

The greater is the absolute price elasticity of demand, the

A) larger is the responsiveness of quantity demanded to the price change. B) smaller is the responsiveness to a price change. C) larger is the income of the buyer. D) higher is the change in demand to an income change.

Which of the following was not a major source of economic growth in the 1920s?

a. construction of residential housing b. production of consumer durables c. railroad construction d. automobile production