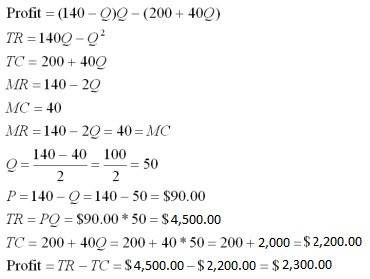

A small fitness center that offers only personal training services has the following demand and cost parameters:Demand: The fitness center has found that it has some discretion in pricing - that is, it can raise price marginally without drastic reductions in volume. Based on statistical estimates of demand and assuming that external factors stay constant (e.g., price of competitors' services, income levels, etc.), the following relationship exists between the hourly rate for a personal training session (P) and the number of sessions demanded per day (Q):P = 140 - Q.Costs: The fitness center finds that its variable costs (e.g., labor) increase at a constant rate of $40 with each additional training session provided per day. Fixed costs such as rent are equal to $200 per day. This yields

the following total variable cost (TVC) and total fixed cost (TFC) equations:TVC = 40Q.TFC = 200.(a) Find the price and quantity demanded (P and Q) that maximize total profit.(b) What is the maximum possible profit?

What will be an ideal response?

The highest possible profit that can be achieved from the profit = total revenue - total cost column is $2,300. This amount can be achieved by charging $90 per session and selling 50 sessions. This managerial decision maximizes profit.

Profit = Total Revenue - Total Cost = (P X Q) - TC(Q) = (P X Q) - (200 + 40Q).

You might also like to view...

Many countries find it difficult to achieve economic growth. This is because economic growth

A) depends on technological change and technological change depends on noneconomic factors such as the growth rate of scientific knowledge. B) is not understood well by economists, so it is difficult to advise policy makers on the best policies to pursue. C) requires saving, and saving means less consumption today. A poor country may find it difficult to consume less today. D) appears to be predetermined and not subject to factors that policy makers can have any affect on.

During an economic expansion as consumer incomes rise, holding everything else constant

A) the demand for most goods, except luxuries, will rise. B) the prices of luxuries will fall while the prices of inferior goods will rise. C) the demand for luxuries and inferior goods will rise. D) the demand for luxuries will rise while the demand for inferior goods will fall.

Irrespective of the market structure, a firm maximizes profit at the level of output where the price of its product equals its marginal cost

a. True b. False Indicate whether the statement is true or false

Diseconomies of scale occur mainly because:

A. Of the law of diminishing returns B. Firms in an industry must be relatively large in order to use the most efficient production techniques C. Of the inherent difficulties involved in managing and coordinating a large business enterprise D. The short-run average total cost curve rises when marginal product is greater than average total cost