Economic incentives can come from

A. taxes.

B. markets.

C. government programs.

D. all of the options are correct.

Answer: D

You might also like to view...

Use the following table to answer the question below. Jane's Production Possibilities SchedulePounds of Green BeansPounds of Corn08020604040602080 0Jane's opportunity cost of producing 1 pound of green beans is ________ pound(s) of corn.

A. 4 B. 1/2 C. 1 D. 2

The process involved in bringing oil to world markets can take years. Substitutes for oil-based products such as gasoline are limited. As a result

A) the supply of oil is very inelastic and the demand for gasoline is inelastic over short periods of time. B) the supply of oil is very elastic and the demand for oil is very elastic over short periods of time. C) the supply of oil and the demand for oil shift to the right over short periods of time. D) the supply of oil and the demand for oil are both perfectly elastic over short periods of time.

The authors of this text argue that oligopolies are interdependent firms. What do they mean by this? Give three examples of the types of interdependence which might occur.

What will be an ideal response?

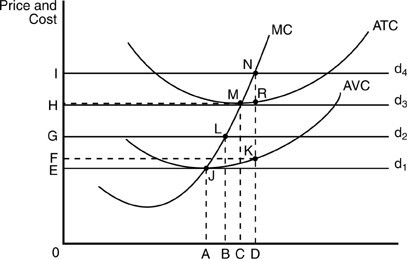

The firm in the above figure breaks even when quantity is

The firm in the above figure breaks even when quantity is

A. A. B. B. C. C. D. D.