If the entry or exit of firms does not affect the resource prices in an industry, we refer to it as a:

A. Fixed-price industry

B. Price-controlled industry

C. Constant-cost industry

D. Price-taking industry

C. Constant-cost industry

You might also like to view...

An increase in ________ reduces the money supply since it causes the ________ to fall

A) reserve requirements; monetary base B) reserve requirements; money multiplier C) margin requirements; monetary base D) margin requirements; money multiplier

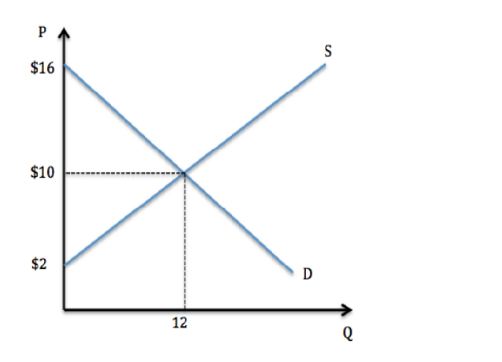

Assume the market was in equilibrium in the graph shown. If the market price were set to $12, which of the following is true?

A. For those still interacting in the market, some surplus is transferred from buyer to seller.

B. For those still interacting in the market, some surplus is transferred from seller to buyer.

C. Producers gain the surplus of those buyers who dropped out of the market.

D. Consumers gain the surplus of those sellers who dropped out of the market.

The price elasticity of demand depends on how readily and easily consumers can switch their purchases from one product to another

a. True b. False Indicate whether the statement is true or false

What is the term for giving up one choice for another opportunity?

a. choice cost b. opportunity cost c. direct cost d. implicit cost e. explicit cost