The monopolist chooses to produce:

A. where marginal cost equals marginal revenue.

B. at a higher quantity than the perfectly competitive firm.

C. at an efficient outcome.

D. at a cost that is equal to a competitive one.

A. where marginal cost equals marginal revenue.

You might also like to view...

Surplus value that is lost due to taxes imposed on imported goods which are keeping the market from functioning as well as it can is called

A) the loss of subsidy. B) the net export deficit. C) rent seeking loss. D) the deadweight loss of a tariff.

A price-taking firm's variable cost function is C = Q3, where Q is the output per week. It has an avoidable fixed cost of $1,024 per week. Its marginal cost is MC = 3Q2. What is the profit maximizing output if the price is P = $192?

A. 0 or 5.33 or 8 B. 5.33 or 8 C. 0 or 5.33 D. 0 or 8

Which of the following is not counted as money?

A. Currency held by the public B. Federal Reserve notes C. Loans made by a bank D. Bank reserves

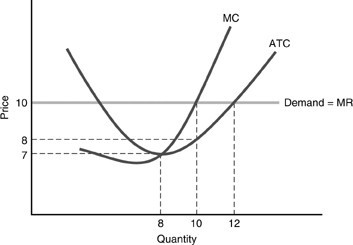

In the above figure, what is the price the firm receives if the output is 8?

In the above figure, what is the price the firm receives if the output is 8?

A. $10 B. $7 C. $2 D. $8