The process of adjustment to a new long-run equilibrium in a perfectly competitive industry is complete when

a. no firms want to enter or exit the industry.

b. every firm has adjusted its production process to make the most efficient use of its resources.

c. investors in the industry receive the standard economy-wide rate of return on their investments.

d. All of the above are correct.

d

You might also like to view...

Refer to Figure 4-1. If the market price is $1.00, what is the consumer surplus on the third burrito?

A) $0.50 B) $1.00 C) $1.50 D) $7.50

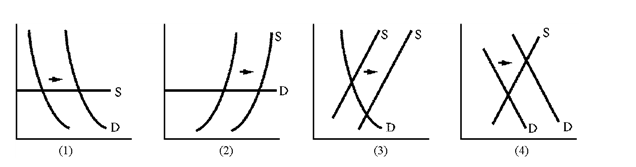

Figure 6-8

Libya sold more crude oil in 1985 than it sold five years earlier, but revenues were 17 percent less. Which graph in Figure 6-8 is consistent with this set of facts?

Libya sold more crude oil in 1985 than it sold five years earlier, but revenues were 17 percent less. Which graph in Figure 6-8 is consistent with this set of facts?

A. 1 B. 2 C. 3 D. 4

Suppose that the quantity of apples sold increases by 30 percent after the price of pears increases by 15 percent. What is the coefficient of cross elasticity of demand?

A. 3.0. B. 1.5. C. 0.2. D. 2.0.

A representative unit by which utility is measured is

A. ordinal utility. B. a util. C. marginal utility. D. utility.