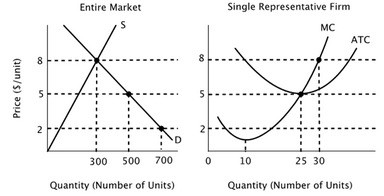

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves. Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

A. It is impossible to determine whether the number of firms in this market will rise or fall.

B. The number of firms in the market will rise as firms enter the market in response to positive economic profit.

C. The number of firms in the market will fall as firms exit the market in response to negative economic profit.

D. The number of firms in the market will not change unless there is a change in either demand or in the cost of production.

Answer: B

You might also like to view...

What alternative to restrictions on capital inflows do some economists recommend to minimize the possibility of increased lending booms and risk taking by domestic banks?

What will be an ideal response?

Subsidizing coal mining and orange growing have both been found to be economically inefficient in that the costs outweigh the benefits. However, a subsidy on coal mining would help the coal producers in West Virginia and a subsidy on orange growing would help the orange farmers in Florida. So the senator from West Virginia approaches the senator from Florida and says that he will vote for the

orange subsidy if the Florida senator votes for the coal-mining subsidy. The Florida senator agrees. Which term best describes what just happened? a. the shortsightedness effect b. logrolling c. the use of user charges d. the political voter theory

If MC = Q/15 represents marginal cost for a monopolist and market demand is given by Qd = 500 - 10P, the monopolist maximizes profit by producing:

A. 500 units of output. B. 187.5 units of output. C. 250 units of output. D. 300 units of output.

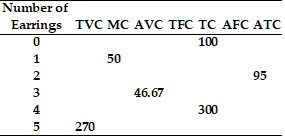

Refer to the information provided in Table 8.2 below to answer the question(s) that follow.

Table 8.2  Refer to Table 8.2. If Sherry produces one pair of earrings, her total variable costs are

Refer to Table 8.2. If Sherry produces one pair of earrings, her total variable costs are

A. $50. B. $100. C. $150. D. indeterminate from this information.